Key Facts

■ Public companies must file regular disclosure documents with the SEC

■ Violations include false statements, misleading omissions, and accounting fraud

■ Financial statement manipulation is among the most common securities violations

■ Whistleblowers often detect these violations through access to internal records

Corporate disclosures and financial violations often relate to false or misleading financial statements that have been filed with the SEC in either a company’s registration statement, prospectus, or as part of any other of the company’s required filings under the Exchange Act.

These violations strike at the heart of securities regulation enforced by the Securities and Exchange Commission. The federal securities laws are built on a disclosure-based system: companies must provide investors with accurate, complete information so they can make informed investment decisions. When a publicly traded company provides false or misleading financial information, they undermine this foundational principle and can cause significant harm to investors who rely on that information. The SEC investigates such securities law violations to protect investors and maintain market integrity in financial markets.

What types of disclosure filings are required by the SEC?

The SEC’s rules cover a wide variety of disclosures. Most notably, public companies are subject to comprehensive requirements governing disclosures they make about their business operations, their financial condition and operating results, and their governance and executive compensation, among other things. SEC rules apply to the disclosure required in a company’s registration statement when the company first goes public. And, after becoming a public company, a corporation continues to be subject to rules requiring annual and quarterly disclosure filings.

Key periodic filings include:

- Form 10-K: Annual report containing audited financial statements and comprehensive business information

- Form 10-Q: Quarterly report with unaudited financial statements and updates on material changes

- Form 8-K: Current report disclosing material events between quarterly filings

- Proxy Statements: Information provided to shareholders before annual meetings, including executive compensation and governance matters

Beyond these periodic filings, companies must also make accurate disclosures in earnings releases, investor presentations, and other public communications about their financial condition and business operations.

Common Types of Financial Statement Fraud

Financial statement manipulation takes many forms. Common schemes that constitute securities law violations include:

Revenue Recognition Fraud:

- Recording revenue before it is earned or realized

- Creating fictitious sales or invoices

- Improperly recognizing revenue from bill-and-hold transactions

- Channel stuffing (shipping excess inventory to distributors to inflate current period sales)

- Round-tripping (circular transactions that create the appearance of revenue)

Expense Manipulation:

- Capitalizing expenses that should be expensed immediately

- Failing to record expenses in the proper period

- Understating reserves or allowances

- Improperly deferring costs to future periods

Asset Overstatement:

- Overstating inventory values

- Failing to write down impaired assets

- Inflating accounts receivable by not reserving for uncollectible amounts

- Recording fictitious assets

Liability Understatement:

- Failing to record liabilities or obligations

- Understating warranty reserves or litigation liabilities

- Off-balance-sheet financing schemes

Violations of the disclosure rules often occur when a company makes false or misleading statements in its public statements or its required SEC filings. Failures to make required filings also fall into this category. One common type of violation is fraud related to a public company’s reported financial results. This type of fraud can occur when a company uses accounting tricks to increase the reported earnings and revenues for a particular reporting period.

Another common scenario is when companies engage in manipulative business transactions that have the effect of altering revenues, expenses, earnings, and/or losses for a reporting period. Sometimes these transactions might even be legal, but they are used unlawfully.

Manipulative transactions designed to meet earnings targets or analyst expectations are particularly concerning and often lead to SEC enforcement actions. These can include:

- Timing asset sales to recognize gains in specific quarters

- Using related-party transactions to inflate revenue or reduce expenses

- Restructuring transactions to achieve the desired accounting treatment

- Cookie jar reserves (building up excess reserves in good periods to draw down in weak periods)

- Improper use of non-GAAP financial measures to obscure true performance

A violation under this category could also occur when a company fails to speak truthfully when discussing its financial results e.g., in press releases or analyst or investor presentations. Additional examples include undisclosed conflicts of interest, corporate governance/legal matters, or the revenue impact of one-time events.

Red Flags Whistleblowers Should Recognize

Individuals working in finance, accounting, internal audit, or operations may observe indicators of possible securities law violations:

Accounting and Financial Reporting:

- Pressure from management to meet earnings targets or analyst expectations

- Unusual or complex transactions near period-end

- Frequent adjustments to financial statements or restatements

- Disputes with auditors about accounting treatments

- Reluctance to provide information to auditors

- Aggressive revenue recognition policies

- Inadequate reserves or allowances

Internal Controls:

- Weak or overridden internal controls

- Lack of segregation of duties in financial reporting

- Management override of established policies

- Missing or altered documentation or records

- Unusual journal entries, particularly at quarter- or year-end

Corporate Culture:

- Emphasis on stock price over business fundamentals

- Unrealistic performance targets

- Retaliation against those who raise accounting concerns

- High turnover in accounting or finance roles

- Lack of transparency with the board or audit committee

Why Whistleblowers are Critical

Corporate disclosure and financial violations are often difficult for the SEC to detect from outside the company. External financial statements may appear compliant while masking underlying fraud or misconduct. SEC whistleblowers with access to internal records, communications, and decision-making processes can provide critical evidence and confidential information that would otherwise remain hidden.

Whistleblowers in these cases often include:

- Accountants and financial analysts who prepare or review financial statements

- Internal auditors who identify questionable practices or possible violations

- Controllers or CFOs who face pressure to manipulate results

- Operations personnel who observe revenue or inventory irregularities

- Compliance officers who identify disclosure failures or breaches of SEC regulations

The insider information these individuals provide can be essential to SEC investigations, often leading to substantial enforcement actions and significant whistleblower awards. Under the SEC whistleblower program, eligible employees and other market participants who report potential violations can receive financial incentives ranging from 10-30% of monetary sanctions collected when their information leads to a successful SEC enforcement action.

The Securities and Exchange Commission has extensive resources and authority to pursue enforcement actions in federal court against companies and individuals engaged in wrongdoing. Penalties for securities law violations can include civil monetary penalties, disgorgement of ill gotten gains, and injunctive relief. In serious cases involving fraud or criminal misconduct, the SEC may refer matters to the Department of Justice for criminal prosecution, which can result in additional criminal penalties and imprisonment for the defendant, including officers who engaged in the violation.

Examples of disclosure violations

Sherron Watkins, the whistleblower in the Enron scandal, is perhaps the most famous truth-teller in history. In 2001, she reported accounting irregularities to the CEO, which ultimately led to the downfall of Enron and its audit firm Arthur Andersen, as well as the indictment of Enron executives. Notably, our practice founder Jordan Thomas was on the SEC team that brought successful enforcement actions against Enron’s attorneys and accountants. Watkins reported internally, but not to law enforcement authorities. Had the SEC Whistleblower Program been in place in 2001, under which Watkins could have reported with anonymity, employment protections, and the prospect of a major financial reward, perhaps the Enron debacle would have played out very differently.

Highlighting the force and effect of the agency’s program, in 2017, the SEC announced a major settlement with Orthofix International, a Texas-based medical device company. Our client—not even an employee, but an outside financial analyst who monitored the company’s reporting—tipped the government to the most serious charges facing the company, accounting failures that caused the company to materially misstate financial statements for years. The misconduct was brought to a screeching halt by the SEC, which levied an $8.25 million penalty against Orthofix.

These cases illustrate that corporate disclosure violations can range from complex accounting fraud affecting millions of investors to specific misrepresentations in periodic filings. Whether the violation involves systematic manipulation of financial results or failure to disclose material information, the SEC takes these cases seriously because they undermine investor confidence and market integrity.

Beyond accounting fraud, the SEC enforcement division pursues various types of securities law violations that harm investors and destabilize financial markets. The agency investigates and prosecutes cases involving insider trading (where individuals trade stocks based on insider information), market manipulation, Ponzi schemes that misuse investor funds, violations of the Foreign Corrupt Practices Act involving bribery, and other misconduct that violates federal securities laws.

For individuals who observe possible securities law violations or potential violations of SEC regulations at their company, it is important to understand the protections and incentives available under the whistleblower program. Speaking with an experienced attorney can help you determine—through a free, confidential consultation—whether the information you have may constitute a reportable SEC violation, as well as provide clarity on the whistleblower process, reporting requirements, and the potential value of a whistleblower claim.

The agency provides significant protections to those who report wrongdoing, including anti-retaliation provisions under the law. Whistleblowers in the securities industry who report violations to protect investors serve a critical role in capital formation and maintaining trust in the public company reporting system. Their complaints and evidence help the SEC pursue enforcement litigation, recover money for harmed investors, and impose consequences on those who breach their duties and engage in trading or other misconduct for personal benefit.

Anyone with knowledge of potential violations should act to protect investors and market participants. The SEC investigation and enforcement process provides multiple avenues for reporting, and the rule of law ensures that those who come forward with credible evidence receive appropriate protections and, in successful cases, financial incentives for their role in exposing fraud and protecting the integrity of financial markets.

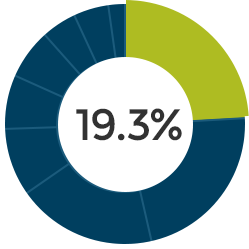

In recent years, on average, 19.3% of all SEC whistleblower tips have involved this type of securities violation.