Whistleblower

Advocates

Award Winning Attorneys

The SEC’s rules cover a wide variety of disclosures. Most notably, public companies are subject to comprehensive requirements governing disclosures they make about their business operations, their financial condition and operating results, and their governance and executive compensation, among other things. SEC rules apply to the disclosure required in a company’s registration statement when the company first goes public. And, after becoming a public company, a corporation continues to be subject to rules requiring annual and quarterly disclosure filings.

Violations of the disclosure rules often occur when a company makes false or misleading statements in its public statements or its required SEC filings. Failures to make required filings also fall into this category. One common type of violation is fraud related to a public company’s reported financial results. This type of fraud can occur when a company uses accounting tricks to increase the reported earnings and revenues for a particular reporting period.

Another common scenario is when companies engage in manipulative business transactions that have the effect of altering revenues, expenses, earnings, and/or losses for a reporting period. Sometimes these transactions might even be legal, but they are used unlawfully.

A violation under this category could also occur when a company fails to speak truthfully when discussing its financial results e.g., in press releases or analyst or investor presentations. Additional examples include undisclosed conflicts of interest, corporate governance/legal matters, or revenue impact of one-time events.

Sherron Watkins, the whistleblower in the Enron scandal, is perhaps the most famous truth-teller in history. In 2001, she reported accounting irregularities to the CEO, which ultimately led to the downfall of Enron and its audit firm Arthur Andersen, as well as the indictment of Enron executives. Notably, our practice founder Jordan Thomas was on the SEC team that brought successful enforcement actions against Enron’s attorneys and accountants. Watkins reported internally, but not to law enforcement authorities. Had the SEC Whistleblower Program been in place in 2001, under which Watkins could have reported with anonymity, employment protections and the prospect of a major financial reward, perhaps the Enron debacle would have played out very differently.

Highlighting the force and effect of the agency’s program, in 2017, the SEC announced a major settlement with Orthofix International, a Texas-based medical device company. Our client—not even an employee, but an outside financial analyst who monitored the company’s reporting—tipped the government to the most serious charges facing the company, accounting failures that caused the company to materially misstate financial statements for years. The misconduct was brought to a screeching halt by the SEC, which levied an $8.25 million penalty against Orthofix.

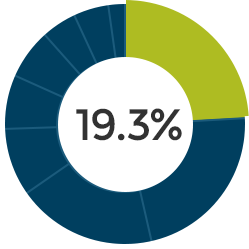

In recent years, on average, 19.3% of all SEC whistleblower tips have involved this type of securities violation.